Types Of Business Ownership

Sole Traders

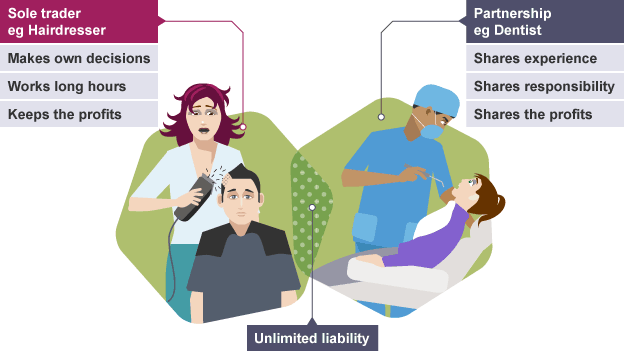

A sole trader is a business run by one person. They can employ workers. Individuals who provide a specialist service like plumbers, hairdressers or photographers are often sole traders.

Sole traders do not have a separate legal existence from the business. In the eyes of the law, the business and the owner are the same. As a result, the owner is personally liable for the firm's debts and may have to pay for losses made by the business out of their own pocket. This is called unlimited liability.

Advantages

A sole trader is a business run by one person. They can employ workers. Individuals who provide a specialist service like plumbers, hairdressers or photographers are often sole traders.

Sole traders do not have a separate legal existence from the business. In the eyes of the law, the business and the owner are the same. As a result, the owner is personally liable for the firm's debts and may have to pay for losses made by the business out of their own pocket. This is called unlimited liability.

Advantages

- Easy to set up

- Small capital investment means reduced start-up costs

- Freedom to make decisions

- Responsibility

- Long hours

- Unlimited liability

Partnerships

Businesses owned by two or more people.

Doctors, dentists and solicitors are typical examples of professionals who may go into partnership together and can benefit from shared expertise. One advantage of partnership is that there is someone to consult on business decisions.

The main disadvantage of a partnership comes from shared responsibility. Disputes can arise over decisions that have to be made, or about the effort one partner is putting into the firm compared with another.

Businesses owned by two or more people.

Doctors, dentists and solicitors are typical examples of professionals who may go into partnership together and can benefit from shared expertise. One advantage of partnership is that there is someone to consult on business decisions.

The main disadvantage of a partnership comes from shared responsibility. Disputes can arise over decisions that have to be made, or about the effort one partner is putting into the firm compared with another.

Limited Companies

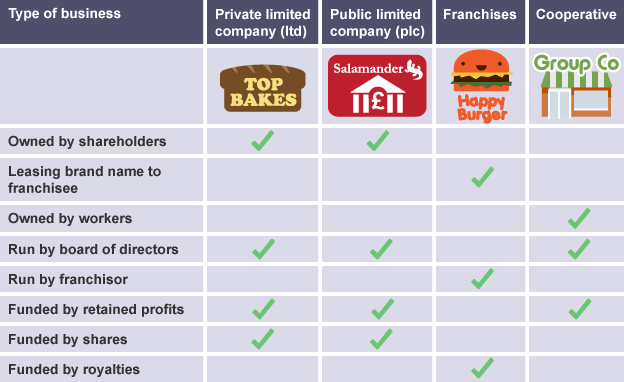

A limited company has special status in the eyes of the law. These types of company are incorporated, which means they have their own legal identity and can sue or own assets in their own right. The ownership of a limited company is divided up into equal parts called shares. Whoever owns one or more of these is called a shareholder.

Because limited companies have their own legal identity, their owners are not personally liable for the firm's debts. The shareholders have limited liability, which is the major advantage of this type of business legal structure.

There are two main types of limited company:

A limited company has special status in the eyes of the law. These types of company are incorporated, which means they have their own legal identity and can sue or own assets in their own right. The ownership of a limited company is divided up into equal parts called shares. Whoever owns one or more of these is called a shareholder.

Because limited companies have their own legal identity, their owners are not personally liable for the firm's debts. The shareholders have limited liability, which is the major advantage of this type of business legal structure.

There are two main types of limited company:

- a private limited company (ltd)

- a public limited company (plc)

Franchising

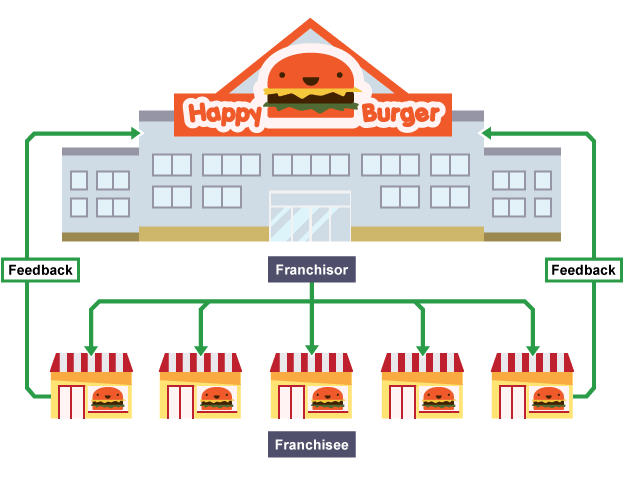

An entrepreneur can opt to set up a new independent business and try to win customers. An alternative is to buy into an existing business and acquire the right to use an existing business idea. This is called franchising.

A franchise is a joint venture between:

An entrepreneur can opt to set up a new independent business and try to win customers. An alternative is to buy into an existing business and acquire the right to use an existing business idea. This is called franchising.

A franchise is a joint venture between:

- franchisee

- franchisor